Paychex Inc released Q4 results on June 25, with the associated 10-K then released on Friday last week (July 11). Our system picked up a number of new flags from the 10-K, pushing the score up from a '7' to our highest risk rating of '10'.

One of the key flags identified was a sharply rising trend in DSO, seen in the chart below (extracted from our automated report).

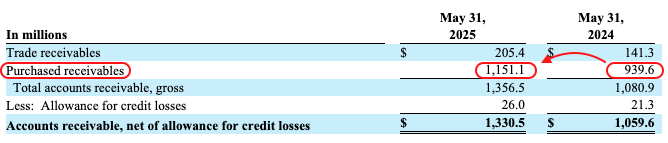

Further investigation into the 10-K reveals that this increase relates mostly to "Purchased Receivables", which have increased by 23% YoY to around $1.2bn. This makes it one of the largest items on the balance sheet (after intangibles, client funds and cash).

Purchased receivables relate to the "Funding Solutions" business, which was described as a distinct business division for the first time in the 10-K for 2025. This business provides "payroll funding" to temporary staffing agencies. These agencies typically incur payroll costs for staff in advance of receiving payment from their own clients. Paychex advances cash to the agency in order to meet payroll costs, with the advance secured against the invoice sent to the end client. The funding is done on a non-recourse basis, meaning that Paychex takes on the credit risk of the end client.

The key subsidiary involved in this business is Paychex Advance LLC, trading as "Advance Partners" (see below). Payroll funding on their website is described as a "creative, flexible way to fuel your staffing firm's growth without the restrictions and red tape of traditional bank loans or lines of credit".

Although there is plenty of disclosure in the 10-K about the funding solutions business, given its growth and size we are surprised that there is only one passing reference to it within the investor presentation and no mention of it on the Q4 earnings call.

Doing a back-of-the-envelope estimate of the contribution of this business, if we assume an average balance of $1bn, a typical discount rate of 4% on invoices and average payment terms of ~42.5 days (consistent with disclosure - see below), this business would be generating around $350m of income per annum (versus ~$4bn of annual revenue for the management solutions business overall). Given sensitivity around growth of the core management solutions business (which slowed to 3% organic in Q4) we think growth of funding solutions should have been given more attention.

While there is nothing inherently wrong with making advances and growing the finance side of the business, this income stream is likely to attract a lower multiple given it requires balance sheet investment (i.e. it is more asset-heavy) and represents a very different risk profile (it is non-recourse).

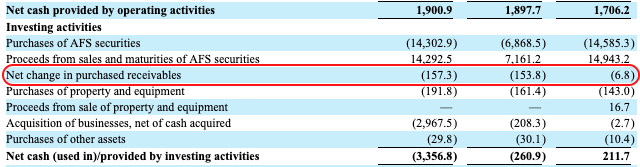

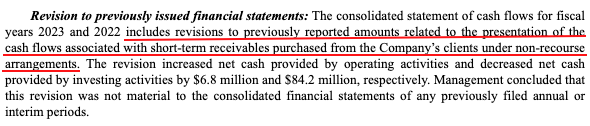

Furthermore, when we look into the cash flow disclosure, we find that growth in purchased receivables is showing up in the "Investing activities" section. Given these advances are part of the ordinary, ongoing business of Paychex, and given the income derived from these receivables is included in revenue, we think it should have been included as part of working capital and presented within operating cash. The impact is not immaterial, since we can see from the cash flow statement there was an associated outflow of ~$150m in both 2024 and 2025 (see extract below).

Interestingly, the presentation of this item was changed in the 2024 10-K, just as these receivables were starting to grow. As seen in the disclosure below (from the 2024 10-K), the company appeared to reclassify these purchases from the operating section to the investing section.

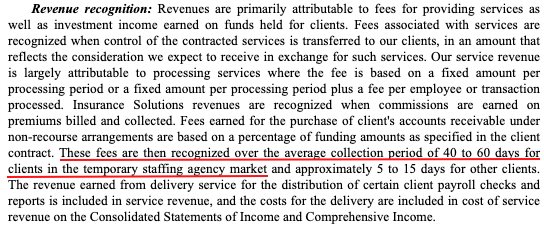

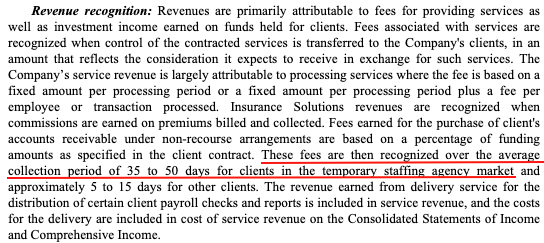

Also picked up by our system, was a change of wording in the accounting policy section for revenue recognition (see extracts below from 2024 10-K and 2025 10-K). This shows that fees earned from the purchase of accounts receivable is recognized over the "average collection period", which has fallen from "40 to 60 days" in 2024 to "35 to 50 days" in 2025. This could reflect a different mix of clients or more stringent requirements being applied in 2025, although the change in collection period is quite drastic. Alternatively this may simply reflect a more optimistic assumption about the average collection period, enabling more aggressive revenue recognition.

2024 10-K

2025 10-K

While expansion of the funding business may be a valid strategy for Paychex, our point is that the market may not be fully aware of the extent of growth in this area given the lack of disclosure outside the 10-K filing. Putting the balance sheet to use like this represents an easy way to grow revenue, but that revenue stream comes with a very different risk profile, particularly in light of rising uncertainty among smaller and mid-sized companies.

Our machine intelligence helps Portfolio Managers to spot critical red flags hidden deep within the financial statements and governance disclosures.

Forensic Alpha uses proprietary machine intelligence to identify risks hidden deep within the financial statements and governance disclosures.

Forensic Alpha Limited

Level 39, One Canada Square

Canary Wharf

London E14 5AB

Forensic Alpha US INC

12 East 49th Street

New York

NY 10017

USA